965 days ago

Leaving LIBOR behind for SORA

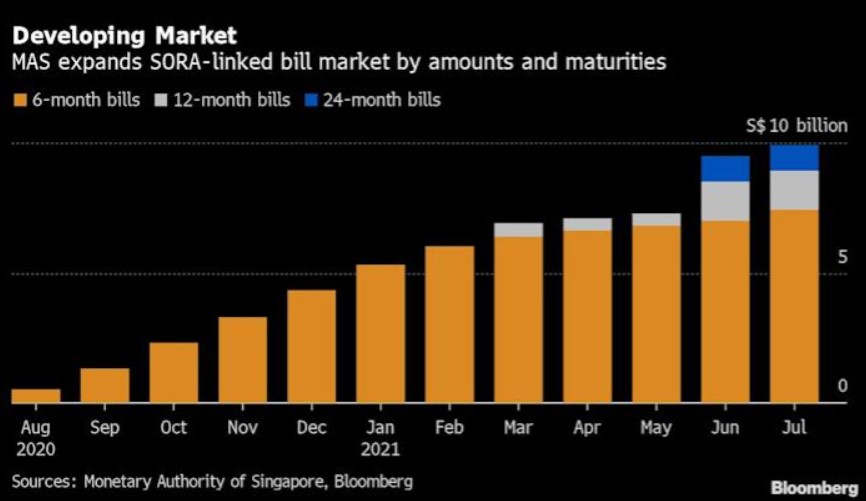

The global reform of benchmark money-market was sparked by evidence emerging in 2008 that European and U.S. lenders had manipulated rates to benefit their own portfolios. Going forward, Singapore dollar-based interest rate derivatives are expected to be predominantly SORA-linked. Since August last year, the Monetary Authority of Singapore has been issuing floating-rate notes that are linked to the new benchmark. The outstanding amount of the securities has soared 20-fold to S$9.9 billion in the past year. Source: Bloomberg